The Solvency II Directive (2009/138/EC) imposes a specific solvency capital charge on currency mismatches between insurance companies’ assets and liabilities. Most insurers choose to hedge the bulk of their foreign-currency exposures unless they hold a particularly strong view on currency valuations, but a 100% hedge will almost certainly fail to yield the best volatility-adjusted portfolio returns over time.

In 2016 we introduced the concept of the Dynamic Ideal Hedge Ratio (DIHR) which showed that volatility-adjusted returns could be improved by taking foreign-currency exposures in a way that was opportunistic and completely integrated into whole-portfolio risk management. In this paper we apply the DIHR to two typical European insurance-company portfolios, one EUR-based and one GBP-based, adjusting the methodology by “handicapping” the expected return of the portfolio’s foreign currency exposures, which is one of the DIHR’s inputs.

We assume an investor considering the DIHR would otherwise choose to allocate solvency capital to the public equity markets, and therefore we apply Neuberger Berman’s long-term annual nominal return estimate for the MSCI World Index as a hurdle rate. We scale this return estimate to reflect the solvency capital ratio applied to this asset class. As such, the DIHR will not recommend the removal of currency hedges unless the case for doing so is compelling from a return-on-capital or diversification perspective, relative to taking public equity exposure.

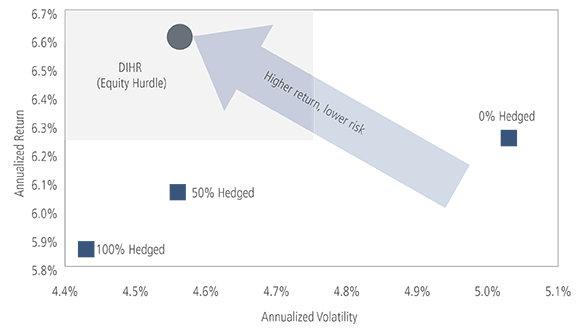

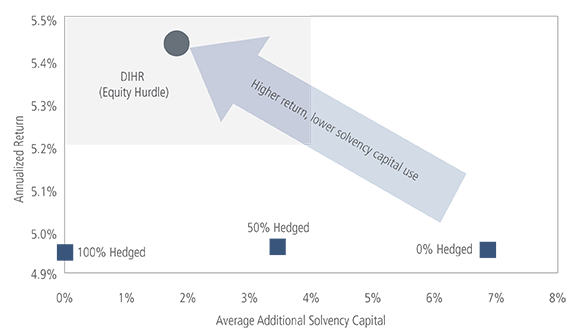

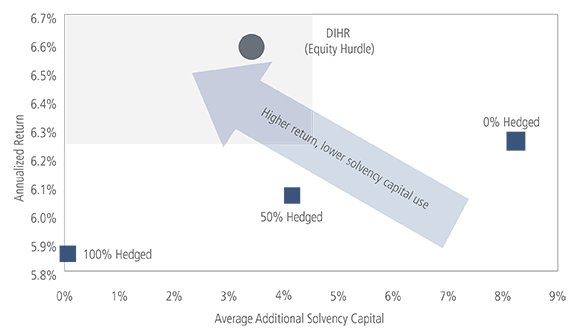

We compare the results with three “benchmark” hedging strategies—100% hedged, 50% hedged and 0% hedged. For both insurance portfolios we show an improvement in volatility-adjusted return, as well as an improvement in volatility-adjusted return for each marginal unit of additional solvency capital required.

In the Appendix we expand our study to show the results for different asset portfolios and different hurdle rates, to show that these improvements are robust to changes in the proxy insurer portfolio allocation, the choice of hurdle instrument and the benchmark hedging strategy used.

We believe we have been conservative in our use of the Solvency II Standard Formula for calculating solvency capital ratios, and we are confident that similar improvements could be delivered for the asset allocation and capital calculation methodologies of specific insurance investors using Internal Models—or indeed for investors with many other kinds of constraints or requirements.

The DIHR Uses Solvency Capital Efficiently in Pursuit of Improved Volatility-adjusted Return

EUR-based insurance proxy portfolio investors

GBP-based insurance proxy portfolio investors

EUR-based insurance proxy portfolio investors

GBP-based insurance proxy portfolio investors

Source: Bloomberg, MSCI, Neuberger Berman Europe Limited calculations. Period under review is 31 January 2003 to 28 February 2018.