Sentiment surrounding emerging markets deteriorated in the first half of 2018, leading to a sell off across the asset class. After adding to positions in the first quarter, JPMorgan data indicate that investors withdrew a net $7.3 billion from emerging markets debt between April and early- July, adding further pressure to the market. Global trade tensions, tariff hikes imposed by the U.S. against its trading partners, tighter U.S. dollar liquidity and signs of softer leading global growth indicators caused mounting concern and revealed the vulnerabilities and dependence on external funding in countries such as Argentina and Turkey.

These risks are worth monitoring, and some areas of the asset class, such as local currency, remain more vulnerable to a deceleration in growth and tighter global liquidity. However, we believe the sell-off has been excessive for hard currency sovereigns, given the solid fundamental profile of emerging markets.

Fundamentals Have Improved, but Valuations Have Deteriorated

The current drawdown in hard currency sovereigns, as measured by the JPMorgan Emerging Markets Bond Global Diversified Index (EMBI GD), has now matched the levels of the “Taper Tantrum” that started in May 2013.

When the U.S. Federal Reserve announced its intention to taper its quantitative easing program, markets were caught off guard. Economies that had enjoyed the tail wind of easy global monetary conditions—especially those having to borrow to finance large current account deficits—were under scrutiny. Spreads widened, and emerging markets currencies depreciated rapidly and the EMBI GD experienced only its second year of negative annual returns since 2003.

Figure 1: Current Conditions Recall the 2013 “Taper Tantrum”

Source: JPMorgan, Bloomberg. Data as of July 31, 2018.

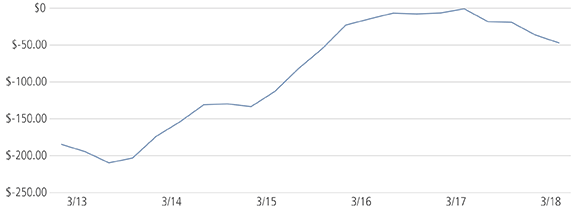

The drawdown year-to-date in 2018 has seen spreads widen and currencies depreciate against the U.S. dollar once again (Figure 1). However, the fundamental profile for emerging markets is stronger than it was five years ago when the so-called “fragile five” economies of Brazil, India, Indonesia, South Africa and Turkey captured the headlines. Current accounts were balanced in 2017, and have only seen a moderate move to deficit in 2018. Compare this to the significant deficit in 2013 (Figure 2).

Figure 2: Emerging Markets External Balance still Favorable in Aggregate

Current account balance for the EM10 aggregate ($bn)

Source: CEIC. The EM10 are Brazil, Colombia, India, Indonesia, Korea, Mexico, Poland, Russia, South Africa and Turkey. China is excluded given its structural external surplus and disproportionately large economy in the context of emerging economies. Data as of March 31, 2018.

In addition, growth in emerging markets has risen and continues to outpace that in developed markets. This year the IMF projects emerging markets will grow by 4.9%, up from previous years, while developed markets can only expect 2.5%. Leading indicators, such as Purchasing Managers Indexes (PMIs), do show some moderation compared to recent data releases, but as of June 2018 they remain above 50 across most emerging markets, indicating continued expansion of business activity.

These dynamics generally support the fundamental strength across emerging markets sovereigns. The ratings profile of the index constituents reflects the fundamental improvement of the asset class over time. By June 2013, 68% of the index constituents by market capitalization were rated investment grade. While this fell to less than 50% as countries were re-rated after the Taper Tantrum, countries that were downgraded to high yield have stabilized their debt profiles and effectively managed through some deterioration, regaining investment-grade status in the process. We think the decline in ratings has bottomed-out and today 50% of the EMBI GD’s market capitalization is rated as investment grade.

An Opportunity to Allocate to a Strategically Diversifying Asset Class

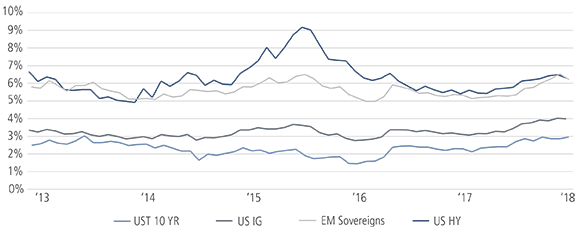

This combination of steady fundamentals and a sharp market sell-off means that valuations in hard currency sovereigns are now attractive compared to their five-year historical average and to similarly rated developed markets spreads. The yield on emerging markets sovereigns remains above the depressed levels of most developed markets, and emerging markets sovereign spreads are now wider even than those of U.S. high yield bonds for the first time in over a decade (Figure 3). U.S. high yield was up almost 1% for 2018 to the end of July, while EMBI GD was down more than 2.5%.

Figure 3: Attractive Valuations

EMD hard currency yields remain attractive relative to the U.S.

Source: JPMorgan, Bloomberg. EM Sovereigns: JPM EMBI Global Diversified Index; US HY: Bloomberg Barclays US High Yield Index; US IG: Bloomberg Barclays US Agg Corporate Index. Data as of July 31, 2018.

EMD hard currency spread minus U.S. high yield spread: EM is wider for the first time since 2005 (Bps)

Source: JPMorgan, Barclays. Indices used: JPM EMBI Global Diversified Index, Barclays US High Yield Index. Data as of July 31, 2018.

There are caveats to mention here—the average emerging markets credit rating has deteriorated a little more than that of U.S. high yield since 2005, and some recent relative underperformance is due to it being a longer-duration market than U.S. high yield, for example.

In addition, the picture is not the same everywhere. Within these market-wide dynamics, there are select countries that active investors could focus to capitalize on these dislocations more fully or with mitigated risk. Countries such as Sri Lanka, Ghana, and Egypt are participating in IMF programs to improve their fundamentals and continue to hit the targets outlined by the IMF, for example. They sold off in the recent correction, nonetheless. Contrast that with certain other countries that have been in the headlines, such as Turkey, where the political tensions have led to significant spread widening, or Argentina, where ongoing reforms led to an acute crisis and the central bank did not react quickly enough to the conditions on the ground.

Nonetheless, valuations at these levels may offer investors an attractive point of entry to establish a position in the asset class or make a relative value trade within their fixed income allocations. This is well worth considering, as emerging markets debt—an opportunity set draws from issuers across more than 80 countries—can be a source of yield that also adds real diversification to a fixed income portfolio. The correlation between emerging markets hard currency and other U.S. dollar-denominated fixed income asset classes since 2003 is shown below (Figure 4). In addition, the asset class may offer fixed income investors an attractive option for return-seeking allocations. Since 2003, the EMBI GD has only seen two calendar years where the total return was negative: 2008 and 2013.

Figure 4: Emerging Markets Offer Diversification in a Fixed Income Allocation

| Correlation | EMD HC Sovereign |

|---|---|

| EMD HC Sovereign | 1.00 |

| Leveraged Loans | 0.41 |

| US Agg | 0.60 |

| US Corp IG | 0.71 |

| US Corp HY | 0.67 |

| UST | 0.43 |

| US Muni | 0.52 |

| S&P 500 | 0.46 |

Source: JPMorgan, Bloomberg. Indices used: JPM EMBI Global Diversified Index, Bloomberg Barclays US Corporate High Yield Index, Bloomberg Barclays US Agg, Bloomberg Barclays Municipal Bond Index, Bloomberg Barclays US Agg Corporate Index, Bloomberg Barclays US Agg Treasury Total Return Index, S&P 500 Index, Credit Suisse Leveraged Loan Total Return. Data as of January 1, 2003 to July 31, 2018.

In conclusion, the recent correction in emerging markets hard currency sovereign debt may provide investors an attractive entry point to establish a strategic allocation to the asset class compared to the past five years, particularly if that allocation is made selectively, based on bottom-up fundamentals. The asset class is certainly at risk in the current geopolitical environment and threats of a trade war, but the sound footing of many countries, and their focus on improving their fiscal and monetary positions, leaves them with more tools with which to weather this tension.