Years of careful planning and diligent investment can be waylaid by a large loss in the critical 10 – 15 years before retirement and have a huge detrimental impact on the longevity of a retiree’s savings.

This risk of experiencing a large drawdown near or in retirement is what drives the long-simmering “to versus through” debate within the target date fund community. “To” target date funds reach their most conservative asset allocation at the point of retirement, having reduced portfolio risk sharply over the previous 10 – 15 years to protect against large drawdowns as that date approaches. “Through” products, in contrast, embrace higher allocations to riskier assets near and even beyond the retirement date in an effort to generate growth and protect against longevity risk (the risk of outliving one’s savings).

At the end of the day, participants nearing retirement need strategies that seek both to mitigate risk and to provide growth potential. We believe replacing a portion of a near-dated target date fund’s equity exposure with a collateralized put write strategy—an option strategy in which the portfolio manager systematically sells fully collateralized short-dated put options on a variety of indexes in an effort to generate equity-like returns with lower volatility over time—can help in this pursuit. Because certain participants may not know how to effectively manage exposure to a put-write strategy, we believe these strategies belong within target date, asset allocation and other professionally managed retirement strategies rather than on a core plan menu.

In this white paper we discuss put write strategies and their potential benefits, explore the importance of providing downside mitigation for near retirees, and illustrate the hypothetical impact of a put write allocation on participant outcomes.

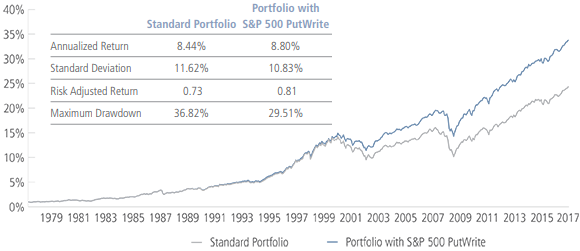

Portfolio with CBOE S&P 500 PutWrite Index Returns Resulted in Improved Return and Less Volatility

Hypothetical Results, Data from 1988 – 2017

Source: Bloomberg. For illustrative purposes only. Asset allocations are rebalanced annually. Asset allocations and performance are represented by benchmarks and do not represent any Neuberger Berman investment product or service. See page 8 of the white paper for allocation weightings and benchmarks. Results shown are hypothetical, do not represent the returns of any particular investment and do not reflect the fees and expenses associated with managing a portfolio. Indexes are unmanaged and are not available for direct investment. Unless otherwise indicated, returns reflect reinvestment of dividends and distributions. Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results.

Note: Descriptions of the Standard and Enhanced TDF glidepaths can be found on page 7 of the white paper.

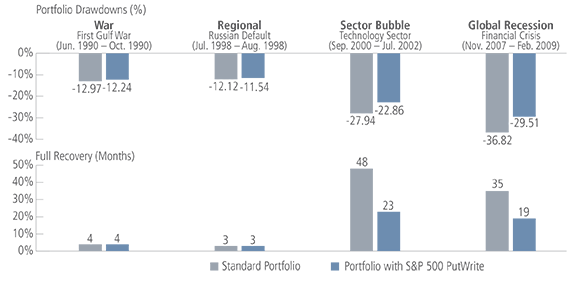

Portfolio with CBOE S&P 500 PutWrite Index Returns Resulted in Lower Drawdowns and Experienced Faster Recovery in Periods of Market Stress

Hypothetical Performance in Periods of Market Stress

Source: Bloomberg LP. For illustrative purposes only. Asset allocations are rebalanced annually. Asset allocations and performance are represented by benchmarks and do not represent any Neuberger Berman investment product or service. See page 8 of the white paper for allocation weightings and benchmarks. Results shown are hypothetical, do not represent the returns of any particular investment and do not reflect the fees and expenses associated with managing a portfolio. Indexes are unmanaged and are not available for direct investment. Unless otherwise indicated, returns reflect reinvestment of dividends and distributions. Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results.