Today’s outlook comes from José Luis González Pastor.

This information discusses general market activity, industry, or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. It is not intended to be an offer or the solicitation of an offer.

1. Could you please set the scene for how PE has performed in Australia and globally over the past 18 months?

During the last 18 months the Australian PE market has continued to demonstrate strong momentum through the COVID-19 period, with annual transaction volumes above pre-pandemic levels. While exits had slowed down in 2020, they rebounded strongly in 2021 in the context of a favorable valuation environment, availability of cheap leverage and significant dry powder. There continues to be strong investor interest in Australia, given the overall resiliency and low volatility of PE investments and the relative under-penetration of the PE market compared to other developed markets globally.

With regards to global markets, 2021 was a record year of Private Equity investments both in terms of capital invested (close to $1,600bn) as well as per deal count c.35,000 transactions with the North American market representing approximately 65% of the buyout activity, one of the largest proportions in the time series of the last decade. For a relative context, capital invested was 50% higher than the prior record pre-pandemic year in 2018. That made the dry powder to yearly capital invested ratio to drop to its lowest level in more than 15 years, to 2.8 years (i.e., assuming the deal making pace of 2021, it would take 2.8 years to invest all the uninvested capital). It has been interesting to see that as of 2Q22, deal making activity globally is still strong, although slightly behind 2021, marking $638bn and c.15,000 investments by private equity. Those figures are still on track to beat 2018 stats. Source: refer to chart below.

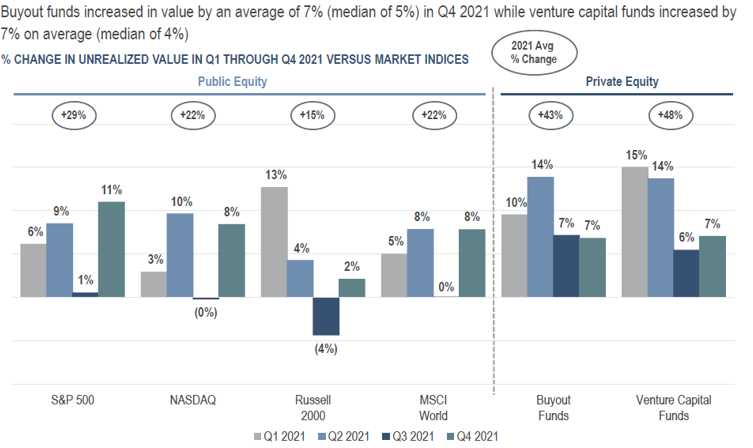

Performance of private equity portfolios in 2021 was very strong. Neuberger Berman’s large portfolios of buyout funds increased in value during the year by 43%. In comparison, the S&P500 was up 29%, the NASDAQ 22% and the MSCI world also 22%. Russell 2000 lagged other stock indexes and went up by 15% in the year. Refer to the source of these figures in this paragraph. Source: refer to chart below.

Summary Findings: Quarterly Performance in 2021

Note: Includes data collected through 1/4/22. Buyout Funds include small-/mid-/large-cap buyout, value buyout (special situations) and growth buyout / growth equity strategies. See additional notes on methodology in Appendix. The benchmark performance is presented for illustrative purposes only to show general trends in the market for the relevant periods shown. The investment objectives and strategies of each fund in the benchmark may be different than the investment objectives and strategies of private equity funds and may have different risk and reward profiles. A variety of factors may cause this comparison to be an inaccurate benchmark for any particular private equity fund and the benchmarks do not necessarily represent the actual investment strategy of a fund. It should not be assumed that any correlations to the benchmark based on historical returns would persist in the future. Indexes are unmanaged and are not available for direct investment. Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results. Nothing herein constitutes investment advice or recommendation. It should not be assumed that any investment objectives or client needs will be achieved.

In the first half of 2022, despite the volatility in capital markets that drove global stock exchanges down, with the S&P500 and MSCI world down 4% in 1Q22 and an additional negative 16% in 2Q22, performance in private equity buyout based on a wide range of buyout portfolios, weathered the storm well, with just a drop of 2% in the first half of the year (vs. the negative 20% of S&P and MSCI). This is a good recent example of some characteristics of the private equity asset class - lower volatility than public markets in turbulent times and attractive performance over time.

2. How are private markets “democratising”?

This term has gained momentum in recent years and refers to the accessibility of private market products that traditionally were only accessible to institutional investors to individual investors.

Historically, across the globe the main hurdles were both regulatory requirements (for instance, the requirement to qualify for a wholesale investor status in Australia) and investment minimums (usually the minimum investing amount is in the millions of dollars).

Today both regulators and fund managers globally are helping individual investors to overcome those hurdles through the launch of suitable products with retail-friendly regulation, it also means offering private market products more accessible or advantageous for investors in a particular jurisdiction. For instance, in Australia Neuberger Berman expects to broaden the offering in the Australian market by launching a local Investment Trust providing access to private equity, mainly through direct investments and secondaries, with the ability to subscribe and redeem on a monthly basis and with a low investment minimum.

3. What trends are you currently seeing within the PE market? What stands out to you?

Neuberger Berman is currently seeing additional selectivity in the buyout market. New buyouts are still happening, but investment firms are carefully selecting the sectors and companies that they want to have exposure to, and valuations are being contested. The pace of deployment has slowed down in the short term compared with 2021 but remains strong in historical terms. Nevertheless, this is the type of environment that may create opportunities for well positioned investors.

In terms of sectors, continuing with the trend accelerated by the lockdowns, Neuberger Berman continues to see significant interest in resilient, cash generative, asset-light businesses and with recurrent or high-level visibility of revenues, such as software, technology, and healthcare, but also sectors disrupted by new technologies such as financial services.

One interesting comparison between current investment opportunities and those from a decade ago or more, is the revenue growth and EBITDA margins of these asset-light businesses. For instance, prior to the GFC a large number of industrial companies were bought and the plan for them to grow was about single digit on an annual basis, and for that it required significant investments in fixed assets, additional investment in working capital and potentially increasing their footprint, with a potential gain of modest improvement in EBITDA margins. Today, many businesses acquired by private equity require limited investment to grow, perhaps more sales teams (think about an accounting software), but don´t have to invest in fixed assets or working capital, so they have significant more free cash flow available than an industrial or traditional company selling goods. Also, their revenues don´t involve any logistic service, as it can be delivered online, so there is no need to worry about energy or oil prices. And usually, they grow faster organically as they can upsell by selling additional add-on services, without any additional cost. Out of this comparison, it stands out that the quality of the businesses targeted today by the private equity industry is of a higher standard than just a decade ago, and not surprising, returns have been very attractive across vintages.

4. What are the benefits of PE investment versus public equities in the current economic environment – rising inflation, interest rates and recession risk?

Private Equity has a number of structural advantages versus public equities which Neuberger Berman believe can be real differentiators in today’s market:

- First, PE makes investments following rigorous due diligence on entry, following access to detailed market and financial information, as well as understanding from management on the areas of improvement and growth. Generally speaking, PE investors have more information and access to management than public investors when making their investment analysis.

- PE investors have the ability to choose the timing of each investment they make given their 3–5-year investment periods and don´t have the pressure to be “invested” like public investors, because the dry powder sits with their investors until it is called, whereas public investors need to put all the capital to work when they receive the flows.

- In the vast majority of the cases, there is control ownership, or at least significant influence, which allow PE owners to implement changes promptly.

- PE has long term objectives and doesn´t have to manage companies to quarterly earnings targets

- Very importantly, good PE firms bring significant operational value add, talent, resources, and expertise to grow the value of the company. Public investors usually are not equipped with these tools and experience and most of the times lack the control to implement any changes.

- Finally, there is the ability to patiently choose exit timing, aiming to sell into strength not weakness, and not having to sell forcedly because of investor´s redemptions, as capital from investors are locked in for a pre-established period of time in the vast majority of private equity funds.

The results and returns that this model has produced over time has led to increasing investor interest and rapid growth of the asset class.

5. What are the pain points investors face in entering private markets?

The main pain point is the limited access to the funds and vehicles of this asset class given the regulatory hurdles (imposing for instance eligibility requirements like “Qualified Purchaser” status in the US or “Professional Investor” status in the EU or “Wholesale Investor” status in Australia) and the minimum commitments. Then, the next pain points are the illiquidity of these products (usually capital is locked for 10 years, although there are distributions over time), the time difference between making the commitment and having all the capital committed actually invested (as usually private funds don´t take the money from investors upfront but rather “calls capital” and usually those calls happen during the 3-5 years that it takes them to put the capital to work). And lastly, the reporting cycle (once every quarter) and method (through a secure platform).

In response to these pain points, a few large managers like Neuberger Berman are offering fully funded vehicles, either with or without liquidity, shorter investment periods and monthly reporting or monthly updates.

6. Do you think there is persistence in private equity returns? If so, why?

Yes, Neuberger Berman strongly believes in the persistence in private equity returns. We have been working with different sides and players of the industry since 2005 and returns have been consistent over time, even during periods of global instability such as GFC, COVID-19 impact, and the war in Ukraine.

There are many reasons that can explain this persistence. I would summarize it thus:

- From the outset, there is a goal from the managers (and an expectation from investors in PE funds) of solid returns in terms of rate of return (IRR) as well as money multiple, generally looking to double the capital invested, and managers are incentivized to achieve these results by means of profit sharing.

- Private equity firms are very selective and so can focus on and look for investment-favorable sectors and great companies, without the limitations of public investors that can only invest in publicly traded companies. So generally speaking, private equity will invest in companies that are already attractive from a revenue and margins profile, discarding “average” or loss-making companies or very competitive or difficult sectors.

- A key value driver of returns for PE is the ability of PE managers to add value to the portfolio companies in multiple ways, from strengthening the management team, to providing resources for growth in new markets or products, to providing strategic guidance and focus, to implementing best practices to increase efficiency and productivity, among others. These combined actions are focused on generating better growth revenues.

- In order to maximise returns, PE managers choose the right time to divest and usually they run a competitive process at exit with several interested buyers. If bids don´t obtain the expected results, private equity managers can wait and sell at a later time and make further improvements or educate future buyers in the waiting time.

- Last to mention, but not least, the companies invested in by private equity managers usually generate significant amount of free cash flow that can serve to paydown debt and increase equity value or even to pay investors a dividend.

7. During this period of volatility, is Neuberger Berman changing its PE strategy? And are you turning your minds to different kinds of deals/assets etc?

Neuberger Berman believes the current environment warrants caution but remains positive on the long-term outlook for private markets. An all-weather strategy can continue to serve our investors well throughout cycles and time.

Neuberger Berman is currently focused on the following secular trends:

- Digitalisation: Corporates & consumers have increasingly embraced digital technologies, accelerated by the pandemic. Neuberger Berman believes these companies are attractive as often they are scalable, provide mission critical services to their customers, have pricing power, and have recurring, predicable and profitable businesses.

- Automation: Automation of industrial processes and services, reducing the dependency on manual labour, enabling efficiency and productivity gains has been another long-term trend.

- Security: As geopolitical tensions have risen, so have security threats. Security is a buzz word across many domains, certainly sovereign and cyber (but also energy, medical equipment, critical inputs, and other). With cyber threats on the rise both in terms of frequency and sophistication, governments, businesses, and communities need enhanced defences.

- Climate solutions and energy transition: The pandemic, extreme weather events and other incidents have exposed the fragilities of our societies, resulting in an enhanced focus on the environment and sustainability by societies at large; increasing a growing need for reliable, cost-effective energy solutions that support growth while simultaneously tacking climate change. This will require substantial investments in electrification solutions, renewables, among others.

- Health & wellness: Another key investment theme. With aging demographics, healthcare systems are increasingly under pressure; at the same time consumers are becoming more health-aware and focused. Solutions that foster efficient, cost effective and broader access to healthcare are in great need. As a result, Neuberger Berman is seeing trends favouring innovation in this sector (such as biopharma, use of AI, developments like mRNA), a higher focus on diagnostics and preventative care (vs treatment), adoption of wearable devices by consumers, and use of telemedicine, outpatient care and other facilities.

- Supply chain reconfiguration: Globalisation is under pressure (from not only nationalistic forces and voices, but largely due to vulnerabilities exposed by both the ongoing pandemic and the conflict in Ukraine). Neuberger Berman is seeing a reconfiguration of supply chains and trading relationships around more regional, and politically aligned clusters. On one hand, the greater automation in industrial manufacturing has reduced the cost gap of production across different geographies; on the other hand, logistical disruptions placed a spotlight on the need for increased supply chain resilience (not just cost). Neuberger Berman expects many industries to be nearshored, and to see significant investments in logistics and supply chain efficiency.

- Evolving labour markets: Unemployment is low in the US, in the UK and across many other developed markets. The shock experience of the pandemic drove many people to reconsider their roles and way of living; government support and buoyant real estate and equity markets over the past two years provided a sense of security to many individuals who left the labour force. With the sharp correction in equity markets, some might reconsider coming back to the work force, but thus far it remains tight. Many of those returning many need to retool themselves and be trained and prepared for the jobs of our decade.

- Rise of global millennial: Finally, the rise of the global millennial, who think, behave, and spend differently. They tend to be more minimalistic, value experiences, engage though social media, and care a lot about sustainability and other factors.

8. How do investors with an ESG or sustainable investment mandate access private deals?

Integrating ESG is a natural fit for private equity investors. Regarding sector focus, private equity managers tend to focus on sectors that are less resource intensive or asset heavy. As such, these also tend to be sectors that are more efficient and experience less volatility, benefitting from secular tailwinds. Moreover, private equity managers are generally able to conduct deep and meaningful due diligence on a company’s specific ESG factors that are financially material. And finally, private equity managers often own and control their portfolio companies and may improve the environmental, social or governance aspects of a company during ownership.

9. Why do you believe super funds are growing their private equity portfolios? And what happens in the event of markdowns?

Private equity has traditionally been an asset class that has exhibited solid annual returns over the long term under most market circumstances and lower correlation in times of market volatility. That’s why it has been present in the portfolios of institutional investors with long term horizons and Super funds can potentially benefit from adding or increasing their allocation to private equity across their portfolios, especially during periods where interest rates provided by fixed income products are significantly lower than inflation.

During periods of decline in value of public markets and public stocks, history has shown that valuations of private equity buyout portfolios also show decline, but this decline in value tends to be smaller (in other words, less losses), bottoming earlier than public markets, and recovering earlier and faster than public markets. This sequence has been the case during the GFC, Neuberger Berman has seen it also during March 2020 with Covid-19 and now during 2022. In the first half of the year main indexes such as S&P500, NASDAQ or MSCI World have declined 20-22% in value, whereas private equity portfolios have suffered on average a 2% decline over the same period of time.