China faces two challenges that are contributing to increased openness in its capital markets—its desire to establish the yuan as a global reserve currency and the need to offset capital outflows that have at times contributed to pressure on the currency. Both require that China attract and retain more non-native assets. Along these lines, the People’s Bank of China took an important step in February when it announced a significant easing of restrictions on foreign participation in the China Interbank Bond Market (CIBM). The PBoC and China’s State Administration of Foreign Exchange (SAFE) then followed up with detailed implementation rules in May and June. Given the noise around these actions, we wanted to provide some clarity on what they could mean for the Chinese debt market and global investors.

Key Developments

- All offshore financial institutions that qualify as medium- to long-term investors can now access the CIBM. Previously only those with qualified foreign investor (QFII or RQFII) quotas could apply. Onshore agent banks will have discretion to assess the eligibility of “medium- to long-term investors.”

- Quota limits have been removed and investors can use their discretion to determine the amount of money they put to work.

- A previous approval requirement has been removed and investors need only file notice of their investment with the PBoC.

- Investors can now access onshore money markets and derivatives including bond repos, bond forwards, forward rate agreements and interest rate swaps for hedging purposes.

- There is no significant restriction on cross-border remittance and no lock-up period. Inflows and outflows of funds can be in the Chinese yuan or in foreign currencies.

All told, this marks the official opening of the onshore bond markets to a large segment of global financial institutions. We believe that most, if not all, “real money” investors will qualify to access the interbank bond market under this scheme. The CIBM handles more than 90% of all onshore bond transactions and foreign investors are now able to access it with relatively few restrictions.

An Important Step toward Bond Index Inclusion

All this increases the probability of onshore Chinese government bonds (CGBs) entering major global bond indices. Following the initial announcement in February, JP Morgan placed the Chinese onshore bond market under review for potential inclusion in its Government Bond Index – Emerging Markets Global Diversified (GBI-EM GD), which is the most widely tracked dedicated EM local currency benchmark. The key items awaiting clarification were:

- The ease of the account opening process;

- Restrictions on entering and exiting the China onshore market, if any; and

- The criteria for defining medium- and long-term investors.

We believe that subsequent detailed implementation documents provided by China have addressed most of JP Morgan’s concerns. So while index inclusion is not yet a certainty, we think it’s reasonably likely that CGBs will be included in the GBI-EM GD over the coming year, especially once the index providers are able to observe the operational effectiveness of new regulations for a few months.

Similarly, CGBs are likely to be considered for inclusion in other major global bond indices, such as the Citi World Government Bond Index and Barclays Global Aggregate Bond Index.

Implications of Potential Inflows

If Chinese government bonds are included in the JP Morgan GBI-EM GD, they will probably come in with a 10% weight, which is the per-country cap in the index. Considering that the size of funds tracking the GBI-EM GD is estimated to be in the region of $180-200 billion (U.S.), such an inclusion will likely bring $18-20 billion of inflows into the China bond markets. Similar analysis shows that inclusion in other global bond indices could lead to another $120-140 billion of inflows, for a total of roughly $150 billion or CNY 990 billion.

While the timeline is still uncertain, and of course depends on actual index inclusion, we believe the bulk of these flows would go through between late 2016 and mid-2018. This view is reinforced by what we consider the relative attractiveness of China onshore bonds. Consider the following:

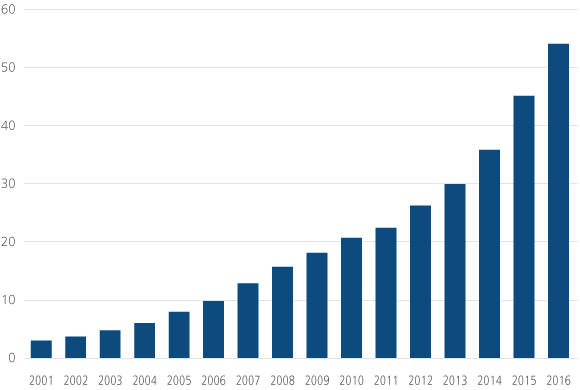

Large market capitalization and fast pace of growth: At approximately $8.3 trillion,1 the onshore yuan (CNY) bond market is the fourth largest2 in the world and has seen rapid pace of growth since the turn of the century. With further financial market reforms and increased local government issuance, we expect this pace to continue in the near term.

Outstanding Volume over Time (CNY trillion)

Source: Haitong Securities. As of April 30, 2016 (latest available)

<!--Source: Haitong Securities. As of April 30, 2016.

*2016 data through April 30, 2016 (latest available).

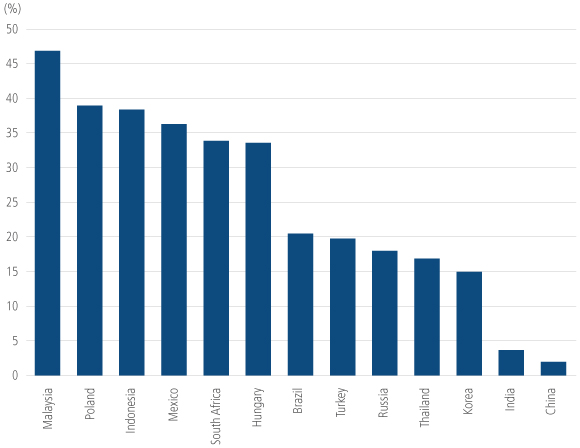

Low foreign investor participation: With foreigners holding only around 2% of the onshore bond market, China ranks poorly in terms of foreign participation within the emerging market universe. Much of this can be put down to access restrictions and non-inclusion in global indices. With both these points being addressed, we expect a significant pick-up in foreign holdings.

Foreign Holdings of Government Bonds (% of outstanding)

Source: Credit Suisse. As of May 31, 2016.

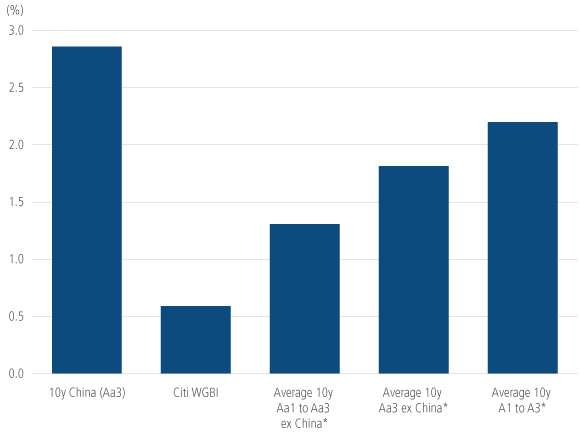

Attractive valuations: In our view, China bonds offer quite attractive yields when compared to their Aa or single A rated peers.

Yield Comparison

Source: Bloomberg, Citi. As of June 30, 2016.

*The averages are of 10-year local government bond yields of countries in the relevant rating bucket as per Moody’s. The countries included are as follows:

Aa1 to Aa3 – Australia, Belgium, Chile, Finland, France, Hong Kong, Qatar, South Korea, Taiwan, United Kingdom Aa3 – Belgium, Chile, Taiwan

A1 to A3 – Bermuda, Czech Republic, Ireland, Israel, Japan, Latvia, Lithuania, Malaysia, Malta, Mexico, Peru, Poland, Slovakia

Given that the annual net supply of CGBs is around CNY 1,400 billion, potential inflows of around CNY 900 billion to CNY 1 trillion would significantly skew supply/demand dynamics in the onshore market. Given a backdrop of accommodative monetary policy, continued moderation in growth and a reasonably steep yield curve, this technical support adds to China government bonds’ performance potential over the next couple of years.

Impact on the Yuan

The prospect of inflows into the local bond market is also a positive for the Chinese yuan, in our view. Set against an estimated current account surplus of $280 billion and a balance-of-payments surplus of $20 billion for 2016, bond-related portfolio inflows in excess of $100 billion can provide a substantial buffer against any renewed capital outflow pressure. We think the prospect of fresh inflows and a strong current account surplus should reduce the risk of a sharp yuan depreciation. That said, policy makers are likely still keen to achieve some gradual weakening of the yuan against a basket of trading partners over the coming year. But in light of the potential improvement in the overall balance of payments, we believe this weakening will be modest, gradual and non-disruptive to financial markets.